- 09/07/2026

- Posted by: Ildar Usmanov

- Categories: Carbon Footprint, Suppluer/Exporter

Internal Carbon Pricing in Malaysia: When GHG Data Needs to Support Business Decisions

Internal carbon pricing in Malaysia is becoming more relevant as companies calculate greenhouse gas emissions, respond to climate-related reporting expectations, and consider how carbon cost could affect business decisions.

For ESG managers, GHG data is often linked to reporting. For Finance, it raises a different question:

What could emissions mean for cost, investment and business risk?

This is where internal carbon pricing becomes more relevant for Malaysian companies that need to connect GHG data with business decisions.

Internal carbon pricing is not the same as an official carbon tax. It is a management tool that helps a company apply a carbon-cost assumption internally, so emissions can be considered in business decisions.

For companies preparing for climate-related reporting, customer carbon requests, export exposure or sustainability-related financing discussions, this can be a practical way to move from GHG data to management action.

Why internal carbon pricing in Malaysia matters now

Malaysia has already signalled a direction on carbon pricing. Budget 2025 announced Malaysia’s intention to introduce a carbon tax for the iron and steel, and energy industries by 2026, with the aim of encouraging low-carbon technologies.

However, companies should not treat any internal carbon price as the official Malaysia carbon tax rate. The final timing, rate and implementation mechanics remain subject to official confirmation.

The stronger immediate business point is simpler:

Even before a final tax rate is known, companies can test how carbon cost could affect decisions.

That is useful for companies with energy-intensive operations, manufacturing facilities, logistics activities, export exposure, or increasing buyer requests for emissions data.

The link with IFRS S2 and climate risk

Malaysia’s National Sustainability Reporting Framework adopts IFRS S1 and IFRS S2 as the baseline sustainability disclosure standards for companies in Malaysia. The framework also follows a climate-first approach and recognises the need for clearer climate-risk and emissions information.

IFRS S2 focuses on climate-related risks and opportunities that could affect cash flows, access to finance or cost of capital over the short, medium or long term. It covers both physical risks and transition risks.

Internal carbon pricing is not required by IFRS S2.

But it can help companies discuss transition risk in a more finance-readable way. For example, management may need to ask:

- Would a high-emission asset remain attractive if carbon cost increases?

- Would an energy-efficiency project look different under carbon-cost assumptions?

- Which products, sites or activities may be more exposed to future carbon-related cost?

- What should be considered in climate-related financial risk discussion?

These are not only reporting questions. They are management and finance questions.

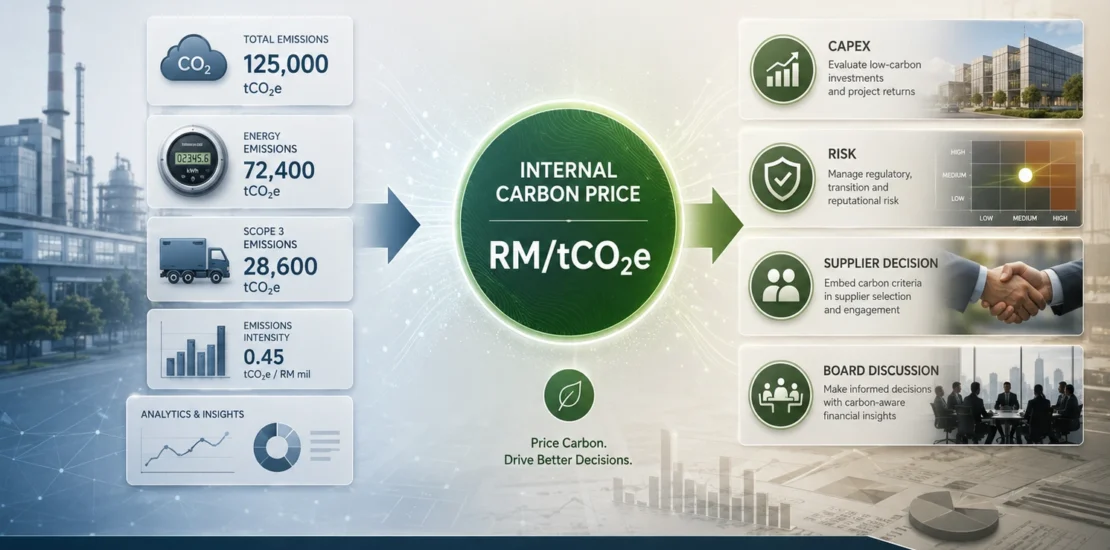

From emissions number to management signal

A GHG inventory shows how much a company emits.

Internal carbon pricing helps management ask what those emissions may mean under different future conditions.

For example, a company may test a notional carbon-cost assumption for Scope 1 and Scope 2 emissions. The point is not to predict the final tax rate. The point is to understand whether carbon exposure could change project priorities, investment timing, supplier decisions or Board discussion.

This can be relevant where companies are considering:

- energy-efficiency upgrades;

- solar or renewable electricity options;

- fuel switching;

- logistics changes;

- supplier engagement;

- product carbon footprint requests;

- climate-risk disclosure;

- green or transition-finance conversations.

For many companies, the first practical step is not a complex internal carbon fee. It is a controlled internal scenario used for selected decisions.

What companies should avoid

Internal carbon pricing can be useful, but it should not become a weak claim.

Companies should avoid presenting internal carbon prices as confirmed Malaysian tax rates. They should also avoid using uncertain GHG data to support strong financial conclusions.

The same caution applies to public disclosure. Internal carbon pricing should not be used to imply compliance, assurance, certification, guaranteed savings, financing approval or buyer acceptance.

Used properly, it is a management tool. Used carelessly, it can create disclosure and expectation risk.

What this means for ESG, Finance and HR teams

For ESG managers, internal carbon pricing can help connect GHG accounting with business decisions.

For CFOs and Finance teams, it can support carbon-cost sensitivity in capex and climate-risk discussion.

For HR and training managers, it points to a growing capability gap.

For Boards and senior management, the useful question is not only:

- What are our emissions?

It is also:

- If carbon had a cost, which decisions would we review differently?

Finance, operations, procurement, facilities and senior management increasingly need to understand how emissions data may affect decisions.

How SuSciCo supports this work

SuSciCo is a Malaysia-based ESG, GHG and carbon consulting and training firm. We support companies that need to strengthen practical understanding of GHG accounting, climate-related disclosure, carbon-cost thinking and sustainability data readiness.

For companies exploring internal carbon pricing in Malaysia, SuSciCo can support discussion at a readiness and management level, including how GHG data may connect with climate-risk discussion, business-case development and IFRS S2-related training needs.

Related support includes GHG Accounting and Scope 3 Training and IFRS S1 and IFRS S2 Training.

This does not replace legal, tax, assurance, verification or financing advice. It helps management, ESG, Finance and operational teams understand the issue clearly enough to ask better questions and prepare more structured next steps.

Is internal carbon pricing the same as carbon tax?

No. A carbon tax is a government policy instrument. Internal carbon pricing is used by a company for internal decision-making. Companies should not present internal assumptions as official Malaysian tax rates.

Does IFRS S2 require internal carbon pricing?

No. IFRS S2 does not require internal carbon pricing. However, internal carbon pricing can support management discussion of transition risk, carbon-cost exposure and climate-related financial effects.

Who should understand internal carbon pricing?

ESG, Finance, operations, procurement and senior management should understand the concept where emissions data may affect capex, customer discussions, reporting, supplier engagement or climate-risk planning.

how can we help you?

Ready to align profitability with impactful ESG strategies? Contact us today to discuss how we can help your business thrive sustainably.

SuSciCo conducted the Life Cycle Assessment in a smooth and efficient manner, making the entire process clear and straightforward for us. The final report was highly informative and provided valuable insights for our work. We truly appreciated their responsiveness, professionalism, and commitment to delivering quality results.

At Zero Waste Earth Store we are incredibly grateful for the exceptional GHG reporting services provided by SuSciCo. Their expertise and dedication played a crucial role in the promotion of our successful recycling campaign. Their accurate measurement and reporting of greenhouse gas emissions allowed us to showcase the significant environmental impact of our recycling efforts. Professionalism, attention to detail, and commitment to sustainability made SuSciCo an invaluable partner in our mission. I highly recommend their services to any organization seeking to make a positive environmental difference. Thank you, Ildar Usmanov, for your outstanding support!