ESG Disclosure Review Malaysia

- 11/05/2026

- Posted by: Ildar Usmanov

- Categories: ESG Reports, Inside ESG Reporting

Sustainability reports are often finalised under pressure, and often, there is no time for ESG Disclosure Review.

The report needs to be completed. Data may still be moving between departments. Management may be reviewing the final draft close to the publication deadline. In many companies, the immediate concern becomes simple:

Is the report ready to publish?

That question matters. But for ESG and sustainability disclosures, another question is just as important:

Are there statements in the report that may create questions later?

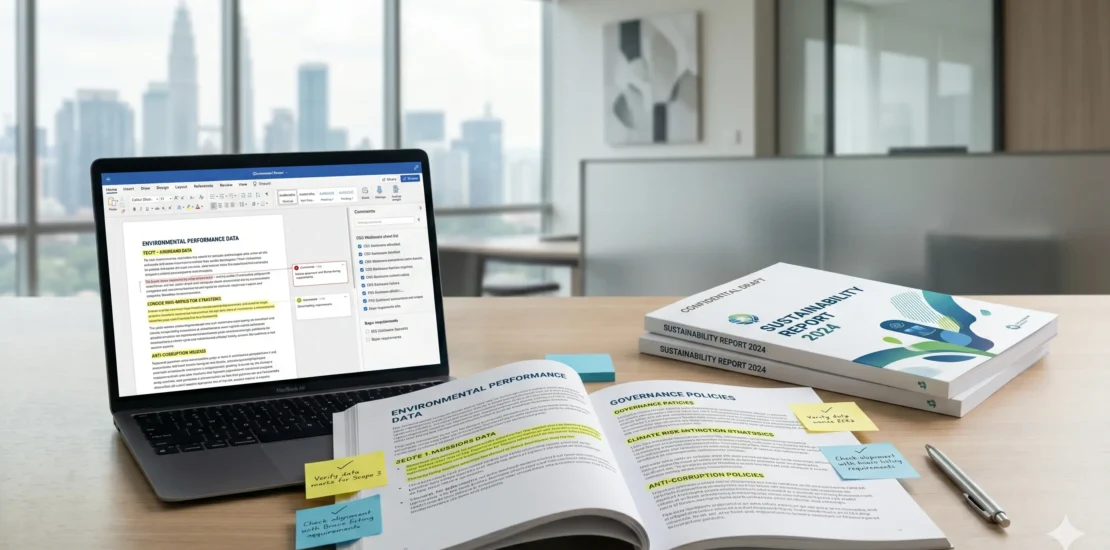

This is where an ESG disclosure review in Malaysia can help companies take a closer look before the report is published or submitted.

Once published, ESG statements can be read by people who were not involved in preparing them. They may be reviewed by boards, management, auditors, lenders, buyers, group offices or future reporting teams. A sentence that looked acceptable during drafting may later be treated as evidence of governance, commitment, capability or performance.

This does not mean companies should avoid ESG disclosure. It means some statements deserve a second look before publication.

Five ESG statements to review before publication

Use the following as recognition points, not a self-review checklist. If these statements appear in your draft sustainability report, they may deserve careful review before publication.

1. Governance claims

Statements about board oversight, management responsibility, ESG committees or decision-making processes can carry more weight than expected.

If the wording sounds stronger than the current governance practice, it may create questions later when responsibilities, meeting records, approvals or internal review processes are examined..

2. Targets and commitments

Targets, goals and commitments can become future accountability points.

A statement that was intended as a direction of travel may later be read as a formal commitment, especially for emissions reduction, waste, energy, supplier ESG, safety, employee development or climate-related matters.

3. Climate and emissions statements

Climate and GHG-related statements often depend on boundaries, assumptions, data quality and calculation choices.

This matters where Scope 1, Scope 2 or Scope 3 information is still developing, or where emissions information may later be used in buyer questionnaires, group reporting or external submissions.

4. Policy and procedure claims

References to policies, procedures, guidelines or internal practices can imply more than intended.

A simple statement about a policy may be read as evidence that the policy is approved, current, applicable and used in practice across the relevant parts of the business.

5. Buyer-facing ESG claims

Some ESG statements do not stay inside the sustainability report.

Language about supplier ESG screening, responsible sourcing, emissions management, product carbon data, safety or environmental performance may later appear in tenders, procurement discussions, ESG rating submissions or customer questionnaires.

The point is not perfection

A sustainability report does not need to describe a perfect organisation.

Many companies are still improving ESG data, internal responsibilities, GHG accounting, supplier engagement, climate understanding and disclosure governance. That is normal.

The better question is whether the report describes the company responsibly.

A useful ESG disclosure should help readers understand what is already in place, what is being improved, what is planned, and what is still developing. It should not make the company appear more mature, certain or committed than it is ready to support.

For many Malaysian companies, the stronger report is not necessarily the longest or most ambitious one.

It is the report that management can understand, support and explain later.

How SuSciCo supports this work

SuSciCo supports with ESG disclosure review in Malaysia, ESG reporting, GHG accounting, Product Carbon Footprint work, supplier ESG responses and practical ESG/GHG training.

Our role is to help companies prepare and review ESG, GHG and carbon-related information with clearer scope, traceable evidence and responsible disclosure boundaries.

SuSciCo does not provide statutory assurance, independent verification, certification, audit, legal compliance confirmation, rating guarantees or buyer acceptance guarantees.

We support preparation and review. Management remains responsible for final disclosures, submissions and external representations.

Need ESG disclosure review support before publication?

If your company is preparing ESG or sustainability disclosures and wants to understand whether key statements may need review before publication, SuSciCo can support a focused discussion.

how can we help you?

Ready to align profitability with impactful ESG strategies? Contact us today to discuss how we can help your business thrive sustainably.

SuSciCo conducted the Life Cycle Assessment in a smooth and efficient manner, making the entire process clear and straightforward for us. The final report was highly informative and provided valuable insights for our work. We truly appreciated their responsiveness, professionalism, and commitment to delivering quality results.

At Zero Waste Earth Store we are incredibly grateful for the exceptional GHG reporting services provided by SuSciCo. Their expertise and dedication played a crucial role in the promotion of our successful recycling campaign. Their accurate measurement and reporting of greenhouse gas emissions allowed us to showcase the significant environmental impact of our recycling efforts. Professionalism, attention to detail, and commitment to sustainability made SuSciCo an invaluable partner in our mission. I highly recommend their services to any organization seeking to make a positive environmental difference. Thank you, Ildar Usmanov, for your outstanding support!